Workers' Compensation Overview

Workers' Compensation Requirement

Customer service representatives must understand the unique concepts that separate each line of insurance. The following are for workers’ compensation.

Compulsory vs. Elective

Workers’ compensation laws are compulsory in almost every state. This means that employers are required to comply with state workers’ compensation laws and must purchase a workers’ compensation insurance policy.

Employers in elective states have the option to enroll in the workers’ compensation system and may elect not to purchase a workers’ compensation insurance policy.

Note: The only elective state Texas.

Policy Providers

In most states, employers have the ability to purchase a workers’ compensation insurance policy from a variety of providers. Policy providers include competitive state funds (state-run insurance companies), private insurance companies, and, in some states, self-insurance (employers’ insurance themselves).

Monopolistic states do not allow for various options as their state laws require employers to purchase a workers’ compensation policy strictly from the state fund. Typically, the state fund policies do not include employers’ liability coverage and a stop gap endorsement (both taught in a future lesson) must be purchased to remove the coverage gap.

Note: North Dakota, Ohio, Washington and Wyoming are monopolistic states.

Failure to Secure Benefits Penalties

There are penalties if an employer in a compulsory state does not secure a workers’ compensation insurance policy. Most penalties are in the form of a fine; however, some states may issue criminal penalties. In addition, most states will also prevent employers from conducting business until the employer purchases a policy.

Exclusive Remedy Provision

Compulsory states often include an exclusive remedy provision within their workers’ compensation statutes. This provision declares that receiving workers’ compensation benefits is considered to be the sole remedy an injured employee has against their employer. In short, injured employees cannot file a lawsuit against their employer for damages.

Workers’ compensation is considered a “no-fault” coverage. This means that an injured worker does not have to prove the employer was at fault for the injury in order to qualify for coverage. In exchange for this, the injured employee gives up the right to sue their employer for damages (as declared by the exclusive remedy provision).

Workers’ compensation coverage consists of three parts:

Part One: Workers’ Compensation

Part Two: Employers’ Liability

Part Three: Other-States

Part 1: Workers' Compensation Coverage

Worker’s compensation coverage provides benefits to employees who are injured or sickened as a result of their employment.

There are four types of benefits employees can receive:

Medical Expenses – Medical cost to treat the injured or ill employee

Disability Income – If the covered injured or ill employee experiences a loss of income, lost wage benefits are paid for.

Rehabilitation Expenses – Physical rehabilitation costs and any associated expenses incurred by the injured or ill employee.

Death Benefits:

Funeral expenses and income stipends for eligible dependents are paid for should an employee’s death occur due to employment.

Workers’ compensation coverage (part one) only provides coverage in the states declared in the policy. However, an unforeseen event or expansion may require an employee to operate in a state not covered by the policy. If the employee is then injured, a workers’ compensation claim could be under the law of another state. If this is the case, a state’s workers’ compensation laws could have higher benefit payouts than the insured’s policy allows for and the insured would be responsible for the difference.

Part 2: Employers' Liability Coverage

Employers’ liability coverage protects the employer in the event an employee makes a claim against them for an injury or illness that is not covered by workers’ compensation laws. Below are a few examples of when this coverage would be used to protect the employer.

Dual Capacity – An injured employee, after filing and receiving benefits for a workers’ compensation claim, also sues their employer for actions other than as an employer. Most often seen as a products liability claim against a manufacturer who is also the employer.

Consequential Bodily Injury – An employee filed a claim against their employer as one of their family members was injured or became ill due to the employee’s working conditions.

Care and Loss of Services (a.k.a. ‘loss of consortium’) – An injured worker files a claim against their employer as they are unable to perform certain home or childcare duties as a result of a workplace injury or illness.

Third Party Over – A workers’ compensation claim is the sole remedy available for an employee injured within the scope of employment. However, in certain situations, the employer may be held liable for additional damages. These are called “Third Party Over” or “Negligence” actions.

It is common in business transactions for contracts to include clauses that require one party (Peter’s Plumbing) to indemnify the other (Gerry the General Contractor [GC]) if that other party (Gerry the GC) is found liable for damages or injuries to third persons. This is called Contractual Liability.

Remember, an injured employee may still claim damages from a non-employer. When an injured employee secures a judgment against a non-employer, the non-employer usually attempts to collect reimbursement from the employer.

When the non-employer uses contractual liability as the reason for reimbursement, it’s called a Third Party Over action.

When no contractual liability exists, a negligence action is filed. (See the Exclusions Lesson for a Negligence Action example.)

Part 3: Other-States Coverage

Workers’ compensation coverage (part one) only provides coverage in the states declared in the policy. However, an unforeseen event or expansion may require an employee to operate in a state not covered by the policy. If the employee is then injured, a workers’ compensation claim could be under the law of another state. If this is the case, a state’s workers’ compensation laws could have higher benefit payouts than the insured’s policy allows for and the insured would be responsible for the difference.

To combat this issue, a coverage-broadening statement can be included in the ACORD 130 (3c) so that the insurance carrier will cover the (potentially increased) amount required for benefits in the non-declared state(s). Here is an example statement,

A policy limit is the highest amount of damages the insurance carrier will pay for a claim that the insured’s policy covers. Workers’ compensation coverage limits vary depending on the state.

Part 1: Workers' Compensation Coverage Limits

There are no set coverage limits for the amount an employee can be paid for Part 1 benefits coverage. As you’ll see later, most other policies have a fixed limit. That being said, it doesn’t mean an injured employee will be paid an endless amount for expenses they incur due to their work-related injury or illness.

Each state has its own method to calculate the amount that will be provided to pay for an injured or ill employee’s benefit expenses. Most often, the following two factors are used somewhere in their calculations:

The employee’s average weekly wage

The severity of the injury or illness

Part 2: Employers' Liability Coverage Limits

Unlike Part 1 of coverage which has no limits, state laws have determined limits for employer’s liability coverage. These limits vary from state to state, but the most common basic limits are:

$100,000 per occurrence for bodily injury

$100,000 per employee for bodily injury by disease

$500,000 overall policy limit for bodily injury by disease

An insured can have these limits increased on their policy by paying an additional percentage on the premium (the percentage amount varies by the insurance company.)

Note: These limits apply to all states except monopolistic states. North Dakota, Ohio, Washington and Wyoming are monopolistic states.

Waiver of Subrogation

A waiver of subrogation is a policy endorsement where one party agrees to waive its right to pursue the other party in the case of a loss.

Example:

A sub-contractor is injured when a general contractor tripped him on the job site, leading to a broken ankle. The sub-contractor’s insurance carrier will pay the benefits owed to the injured employee and then pursue the general contractor’s insurance carrier for the paid loss amount. A waiver of subrogation in favor of the general contractor will prevent the sub-contractor’s insurance carrier from recovering the paid loss amount.

Waiver of Subrogations can be issued in two different versions.

A blanket waiver of subrogation provides the ability to issue an unlimited amount of waivers at a fixed cost (usually 2% of annual premium). This also expedites the process for issuing waivers on certificates of insurance.

Common Workers’ Compensation Exclusions

Aircraft Operation – All members of the flying crew like pilots, navigators, etc. are excluded

Foundry Operations – Those involved in melting and pouring the metal into the mold or other parts of the foundry operations process are excluded

Asbestos Abatement – Those involved in the procedures designed to control the release of asbestos fibers from asbestos-containing materials are excluded from

Daycare Services – These are excluded if daycare services are provided by the insured primarily for use by its employees’ dependents

Also known as a ‘Project Specific’ waiver of subrogation. As the name infers, it is issued on a project-specific basis. This option is more common when the insured needs to issue fewer waivers on a policy. The cost is typically 5% of the premium generated for the project, and often takes a few days and some paperwork to get issued.

DID YOU KNOW?

Waivers of subrogation can only be issued by an insurance carrier, but you will most likely get asked by an insured to provide one. When this happens, check to see if the insured has a blanket waiver of subrogation already on their policy. If so, you can provide the waiver of subrogation via a certificate of insurance. If not, you will need to request that the insured’s insurance carrier issue a waiver of subrogation.

Common Endorsements

Stop Gap (Employers’ Liability) Endorsement

Employers in monopolistic states must purchase workers’ compensation insurance from the state fund. The state fund policy does not often cover all of the employer’s liabilities which are required and automatically included in non-monopolistic states.

Since this is the case, employers in monopolistic states doing business in non-monopolistic states must obtain the additional required employers’ liability coverage to be in compliance. To do so, a “stop gap” or “employers liability coverage gap” is usually attached with their state fund insurance policy. The stop gap employers’ liability endorsement fills in the state fund’s employers’ liability coverage (Part 2) gap that is required by the non-monopolistic states.

Voluntary Compensation Endorsement

In some states, workers’ compensation insurance is not required for employers who have fewer than a specified number of employees. In other states, employees are classified in a category making them ineligible for coverage by workers’ compensation insurance. A voluntary compensation coverage endorsement allows the employer to extend workers’ compensation insurance benefits to these types of employees. If these types of employees are then injured on the job, they have the option to either volunteer for the extended benefits coverage or file a lawsuit against the employer.

Other Endorsements

We will not be covering these endorsements as their applications vary by state. We recommend working with a supervisor should you come across any of the following endorsements.

Employee Leasing Endorsements

Alternate Employer Endorsement

Employee Leasing Client Endorsement

Employee Leasing Client Exclusion Endorsement

Labor Contractor Endorsement

Labor Contractor Exclusion Endorsement

Federal Endorsements

Federal Employers’ Liability Act Coverage Endorsement

Longshore and Harbor Workers’ Compensation Act Coverage Endorsement

Outer Continental Shelf Lands Act Endorsement

Maritime Coverage Endorsement

Defense Base Act Coverage Endorsement

International Endorsement

Foreign Coverage Endorsement

Common Exclusions

An exclusion is language in an insurance policy that, instead of adding or modifying coverage, removes coverage from the policy. This is sometimes built into the policy language itself, but oftentimes by endorsement. If the excluded coverage is necessary for the insured, the insured can sometimes negotiate for the exclusion to be removed from the policy.

Common Workers’ Compensation Exclusions

Aircraft Operation – All members of the flying crew like pilots, navigators, etc. are excluded

Foundry Operations – Those involved in melting and pouring the metal into the mold or other parts of the foundry operations process are excluded.

Asbestos Abatement – Those involved in the procedures designed to control the release of asbestos fibers from asbestos-containing materials are excluded from

Daycare Services – These are excluded if daycare services are provided by the insured primarily for use by its employees’ dependents

Employers Liability Insurance Exlusion

The first exclusion under Employer Liability Insurance excludes coverage for “liability assumed under a contract.” This means that coverage for Third Party Over actions has been removed and is NOT covered by the Workers Compensation/Employer Liability Insurance form.

Mike operates the hydraulic press for a car manufacturing plant. The press has a history of malfunctioning. The press malfunctions and injures Mike. Although Mike suffers a work-related injury, he sues the manufacturer of the hydraulic press and collects damages. The manufacturer of the hydraulic press then sues the car manufacturing plant for allowing Mike to continue to operate an unsafe machine.

Since there was no contract requiring indemnification by Mike’s employer, this is a negligence action and would be covered under the employer’s Employers’ Liability Insurance policy.

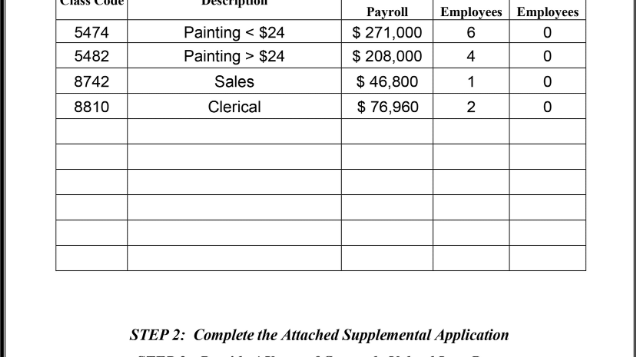

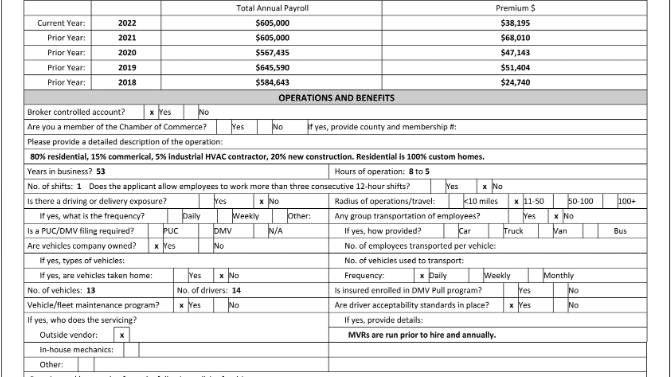

Annual payroll figures are key to understanding an insured’s business operations and the size of their workforce. Insurance carriers require these figures to accurately calculate the policy premium. Since the policy will be providing coverage for a future period, it is necessary for an insured to provide their estimated annual payroll figures.

Most often a document is sent to an insured to receive their estimated annual payroll figures.

Estimated annual payroll figures are broken down by class code. This allows insurance carriers to better understand an insured’s business in more detail and the exposure for each job duty. A policy’s premium will be lower if an insured’s workforce is 90% clerical rather than 90% electrical.

The number of full and part-time employees is also important. Whether or not an insured has six full-time employees doing a job versus 12 part-time employees doing the same job impacts the policy premium.

DID YOU KNOW?

It will be common for you to be asked estimated payroll questions from an insured. Most often it is regarding the correct way to calculate their estimated annual payroll figures. Unlike most, the insurance industry calculates payroll figures using straight time wages rather than gross wages.

Straight Time Wage

In the insurance industry, concern is mostly placed on an insured’s level of exposure rather than the extra amount paid to an employee for overtime. This translates to insurance carriers wanting to know:

How many hours were worked by an insured’s employees (including overtime hours)

Payroll estimates based off of regular pay rates NOT overtime pay rates

When these rules are used in calculating the estimated payroll figures for an employee, the outcome is considered the employee’s straight time wage.

Note: Estimated payroll figures are the sum of an insured employee’s straight time wages grouped by class code. This means an insured must calculate every employee’s straight time wage and then add them all together.

Calculating Straight Time Wage

An employee’s straight time wage calculation involves taking their gross wage and reducing it down to what it would have been if only the regular pay rate had been applied. The amount of wage reduction for the calculation depends on the overtime rate used to calculate the gross wage for the employee:

If the employee received time and a half (1.5 X regular pay rate), then we must divide the employees annual overtime pay by 1.5 and add the result to the regular time wages.

If the employee received double time (2 X regular pay rate), then we must divide the employees annual overtime pay by 2 and add the result to the regular time wages.

The best way to help better understand this concept is by working with an example.

An employee’s gross wages for the year was $55,000. The employee’s regular pay rate was $20/hr., but was paid at time and a half for 500 overtime hours worked. What are the employee’s straight-time wages?

Overtime Pay

First, calculate the employee’s overtime pay rate.

$20/hour X 1.5 (time and a half) = $30/hour

Second, calculate the employee’s total overtime pay for the year.

$30/hr. x 500 overtime hrs. = $15,000

2. Apply the Regular Pay Rate

Now that you know how much was paid for overtime, the next step is to determine how much would have been paid if only the regular pay rate was applied (remember, insurance carriers don’t want overtime included in payroll.)

$15,000 / 1.5 (time and a half) = $10,000

3. Reduction Amount – Calculate the Non-Included Overtime Pay Amount

The next step is to determine how much the overtime pay rate increased the employee’s gross wage.

$15,000 – $10,000 = $5,000

4. Calculate the Employee’s Annual Straight Time Wages

The last step is to reduce the employee’s annual gross wage by the amount it was increased due to overtime.

$55,000 – $5,000 = $50,000/year

Remuneration vs Payroll

Payroll (straight time wages) makes up the majority of the estimated ‘payroll’ figures, but it is more accurate to have an insured estimate their remuneration figures.

The following details what is and is not included in remuneration.

Wages or salaries including retroactive wages or salaries (payroll)

Total cash received by employees for commissions and draws against commissions

Bonuses including stock bonus plans

Extra pay for overtime work

Pay for holidays, vacations, or sick days

Annuity plans

Payment or allowance for hand tools or power tools used by hand provided by employees used in their work or operations for the insured

The rental value of an apartment or a house provided for an employee based on comparable accommodations

The value of lodging, other than an apartment or a house, received by employees as part of their pay, to the extent shown in the insured’s records

The value of meals received by employees as part of their pay to the extent shown in the insured’s records

The value of store certificates, merchandise, credits, or any other substitutes used for money received by employees as part of their pay

Payments for salary reduction, retirement, or cafeteria plans that are made through deductions from the employee’s gross pay

Davis-Bacon wages paid to employees or placed by an employer into third-party pension trusts

Expense reimbursements to employees to the extent that an employer’s records do not substantiate that the expense was incurred as a valid business expense

Payment for the filming of commercials excluding subsequent residuals which are earned by the commercial’s participant(s) each time the commercial appears in print or is broadcast

Payment by an employer of amounts otherwise required by law to be paid by employees to statutory insurance or pension plans, such as the Federal Social Security Act

ips and other gratuities received by employees

Payment by an employer to group insurance or group pensions plans for employees

The value of special rewards for individual invention or discovery

Dismissal or severance payments except for time worked or for accrued vacation

Payments for active military duty

Employee discounts on goods purchased from the employee’s employer

Expense reimbursements to employees to the extent that an employer’s records substantiate that the expense was incurred as a valid business expense

Sick pay paid to an employee by a third party such as an insured’s group insurance carrier that is paying disability income benefits to a disabled employee

Supper money for late work

Work uniform allowance

Employer-provided perquisites (“perks”) such as:

An automobile.

An airplane flight

An incentive vacation (e.g., a contest winner)

A discount on property or services.

Club memberships

Tickets to entertainment events

- Employer contributions to salary reduction, employee savings plans, retirement, or cafeteria plans – contributions made by the employer, at the employer’s expense, that are determined by the amount contributed by the employee.

Independent Contractors vs Employees

An independent contractor is a natural person, business, or corporation that provides goods or services to another entity under terms specified in a contract or within a verbal agreement. Unlike an employee, an independent contractor does not work regularly for an employer and is usually paid on a freelance basis. Independent contractors often work through a company or franchise, which they themselves own, or may work through an umbrella company.

Below are lists of helpful information to guide you and the insured in determining whether or not a worker should be classified as an independent contractor or employee.

The insured pays them and they do not have a license, but are required to have one

The insured supplies the tools, the work is performed on the insured’s premises and at the direction of the insured

They are paid through commissions, piecework or by the hour

They are paid on a ‘by-the-job’ basis

They perform work in the same capacity for other businesses

Whether or not the work is a part of the regular business of the principal or alleged employer

The alleged employee’s investment in the equipment or materials required by his or her task or his or her employment of helpers

Whether the service rendered requires a special skill

The alleged employee’s opportunity for profit or loss depending on his or her managerial skill

The length of time for which the services are to be performed

The degree of permanence of the working relationship

Whether or not the parties believe they are creating an employer-employee relationship may have some bearing on the question, but is not determinative since this is a question of law based on objective tests.

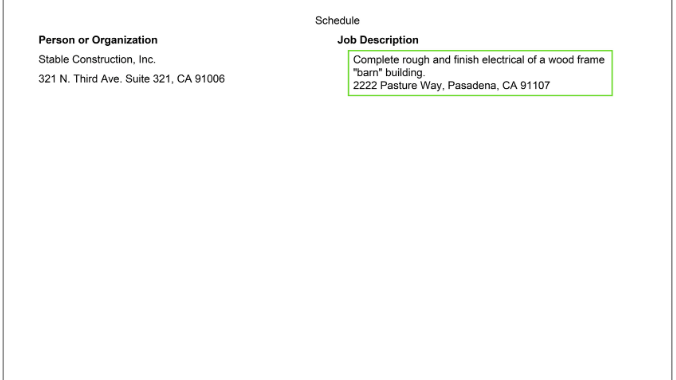

ACORD forms provide the majority of information needed for an insurance carrier to write a policy. However, insurance carriers may still require additional information regarding the insured’s business operations as it relates to their industry. Supplemental applications are what provide this additional information to the insurance carriers.

When required by an insurance carrier, either the producer or the customer service representative will send a supplemental application to an insured for them to complete.

Additional information that the insured may provide for a workers’ compensation insurance policy include:

Operations relevant to workers’ compensation coverage

Scope of work

Safety procedures

Hiring practices

Payroll history

Any other details not found on ACORD forms, but are necessary for the insurance company

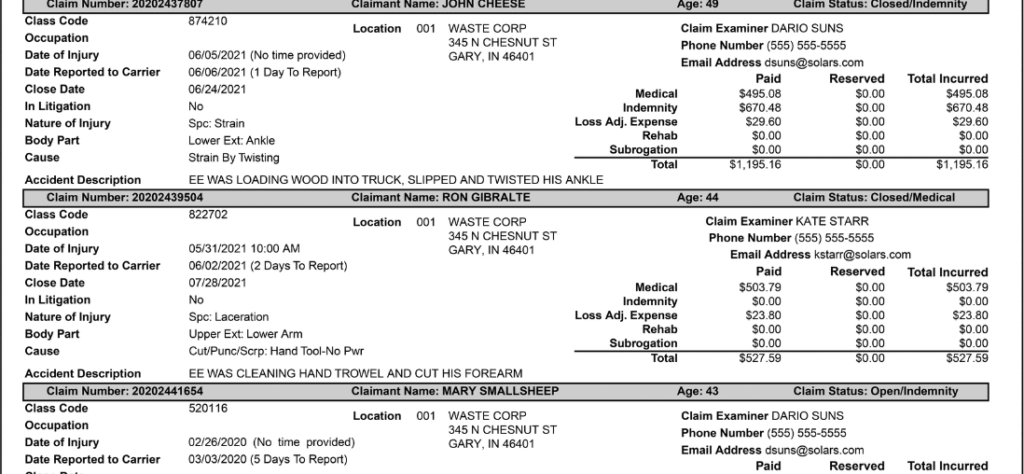

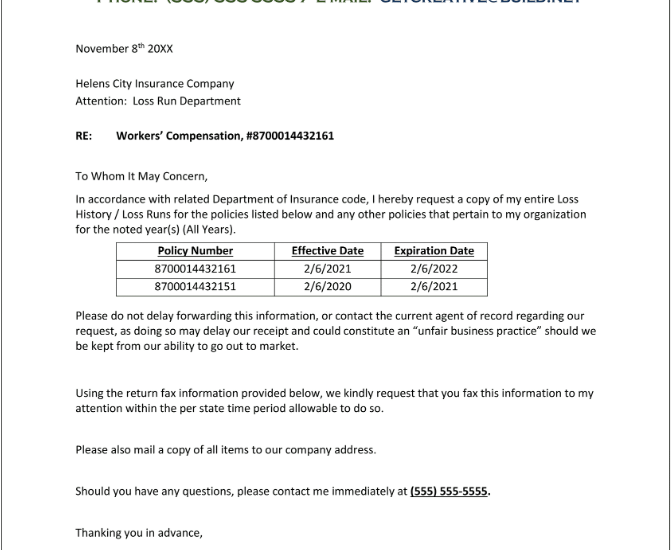

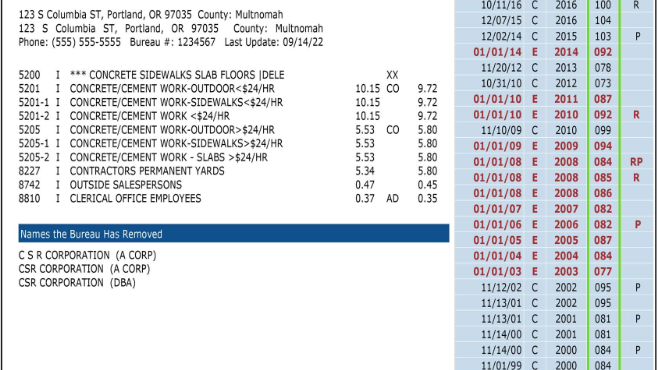

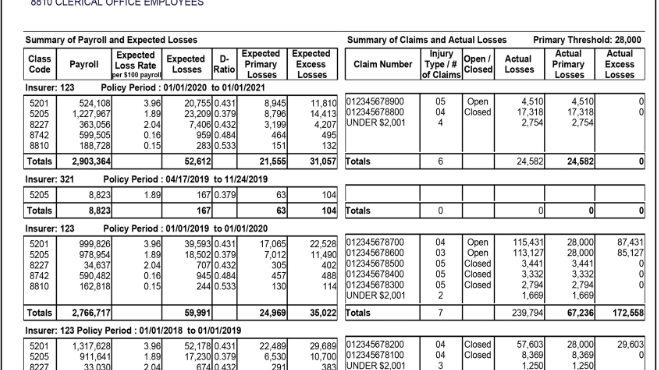

Currently Valued Loss Run Reports

An insured’s policy history is another critical piece of information an insurance carrier needs to accurately calculate a policy premium. A loss run report provides insurance carriers with an insured’s specific policy period history. Insurance companies use loss run reports to better assess the risk of an insured and typically use the last five policy periods in their policy premium calculations.

Sample Loss Run Report

A currently valued loss run report means the claims information has last been updated within 90 days of the policy’s expiration. Otherwise, most insurance companies would not accept the loss run report.

Note: Loss run reports can vary immensely from one insurance company to another.

Loss run reports must be requested from the insurance carriers who wrote each of the insured’s policies over the last five policy periods (if applicable).

In order to release the information, the insurance carriers need to receive an agent of service authorization letter from the insured. The letter provides permission for the insurance carrier to release the insured’s loss run data, most often, to the insured’s current agent of record (you).

The insurance policy carrier is bound by law to provide the loss run report within a certain period of time (dependent on the state). This is state-regulated to ensure that the insured has the freedom to shop for more affordable insurance policies.

DID YOU KNOW?

If the insured has an excellent claims history, you can negotiate with insurance carriers to provide the insured with discounted premiums.

Experience Mods (X-Mods) are rating factors used to compare an insured’s claim and payroll history against other employers with similar operations. Insurance companies use it as an indicator to determine how well the insured manages the risks correlated to what they do. Depending on the rating, X-Mods adjust the insured’s policy premium positively or negatively. Another way of looking at it, X-Mods are an incentive for insureds to create better working environments to lower or completely avoid employee-related injuries.

Understanding Experience Modification Rates

EMR calculations include an insured’s payroll and loss history. The experience rating period used in X-Mod calculations generally consists of three full years, ending one year prior to the effective date of the modification. Payroll and losses from the most recent year are not considered to be credible for rating purposes and are not used in rating calculations.

Example

If the experience modification is effective January 1, 2022, the experience modifier will reflect payroll and loss experience between January 1, 2020, and January 1, 2021.

Below are flashcards showing you how to interpret the different experience modification ratings insureds can have

Obtaining Experience Modification Ratings

An insured’s EMR can be obtained from two possible sources: an X-Mod history report or an X-Mod worksheet.

Most insurance agencies or companies provide customer service representatives access to a system to look up an applicant’s EMR. If this applies to you, ask a supervisor to better understand how to pull this information.

The National Council on Compensation Insurance (NCCI) is the bureau specializing in workers’ compensation. Most states follow the NCCI standard for X-Mod rating calculations; however, other states (such as California) do not.

Workers Compensation Benefits

Workers' Compensation Ex-Mod Explanation

Premium and Rate Summary

Premium Rating Detail

State Assessments

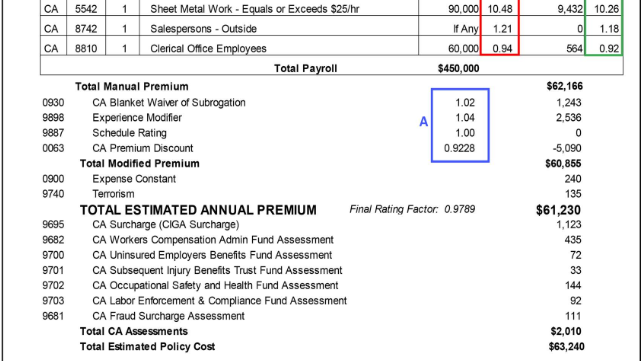

Calculating Net Rates

Not all the policy quotes provided by the insurance carriers will include net rates. Understanding how to calculate net rates is important. Net rates are included in policy proposals as they allow the insured to compare their policy quotes from different carriers, or from one year to the next, and reflect the actual rate per $100 in payroll the insured will be charged.

A – Multiply all ratings against each other to get your ‘combined rate’

B – For each class code, multiply the ‘base rate’ by the ‘combined rate’

C – The result is each class code’s ‘Net Rate’

Example – Class Code 5538:

(1.02 X 1.04 X 1.00 X 0.9228) X 17.39 = 17.02

Note: All insurance carriers and agencies calculate their net rates differently. What has been provided is the most basic formula. We suggest working with your supervisor to better understand how you should be calculating net rates for your policy proposals.

State Assessments

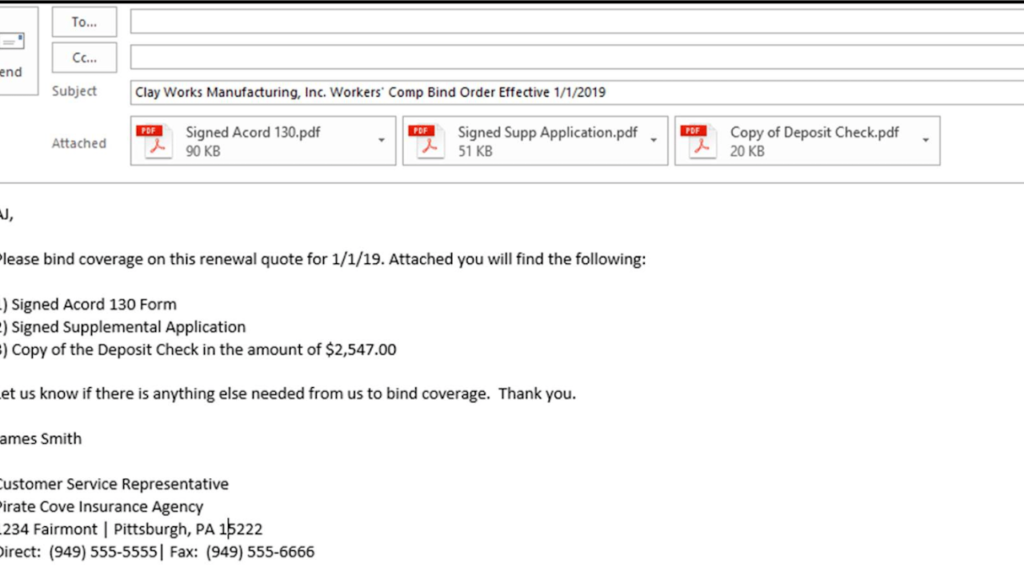

Binding coverage means that an applicant has agreed to an insurance company’s quote and is requesting that the coverage begins on the policy’s effective date. This request to bind coverage is referred to as a bind order.

Bind Order

Insurance carriers require customer service representatives to submit bind orders in writing. Bind orders can be submitted via mail, email, fax or through an insurance carrier’s online system (if available).

Signed ACORD 130 form

Signed supplemental application(s)

A copy of the deposit check

Subjectivities (other forms as required by the insurance carrier)

Policy Checking

The insurance carrier will issue the policy within two to four weeks after coverage is bound. In most situations, the customer service representative will be sent the policy before it is sent to the insured. It is critical to check the policy for accuracy and resolve any discrepancies with the insurance carrier prior to sending the policy to the insured.

The QUOTE, including revisions, provided by the insurance carrier

The PROPOSAL provided to the insured

The POLICY being issued

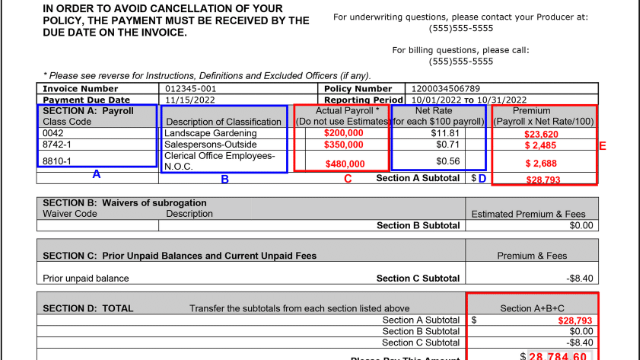

Understanding a Monthly Payroll Report

Sometimes an insured asks for a customer service representative’s assistance when completing the monthly payroll report. Below is an example monthly payroll report and how to understand its contents:

Blue = Information provided by insurance carriers

Red = Information provided by the insured

A – Class Code: This information can be found in the insurance policy quote and pertains to the various job duties the insured has exposure to.

B – Classification Description: A specific description to help clarify the job duties the class codes reference.

C – Actual Payroll: Also known as gross payroll (total employee wages before taxes and other deductions). Totals are for the reporting period in each appropriate class code.

D – Net Rate: Determined via the policy quote for each class code. It is the amount the insured is being charged per one hundred dollars of payroll/remuneration.

E – Premium by Class Code: The cost for the insured per class code for the reporting period.

F – Monthly Premium Due to Insurance Carrier: The final monthly premium (cost) the insured owes to the insurance carrier for their insurance policy.