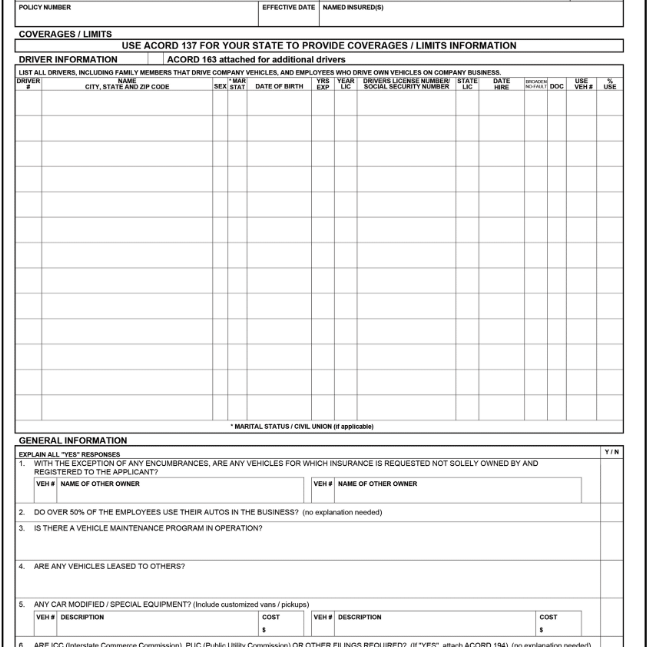

Named Insured

The individual or company listed as the named insured

Permissive Users

Individuals the named insured has provided permission to operate autos covered by the commercial auto policy

Omnibus Insureds

Individuals who are legally liable for the conduct of either the named insured or the permissive users